If you've registered a US LLC as a non-resident and own 100% of it, this article applies to you directly. Form 5472 isn't a "maybe if you have operations" — it's an annual mandatory filing. Most clients learn about it after the fact, often after their first missed deadline.

What Form 5472 is and why the IRS requires it

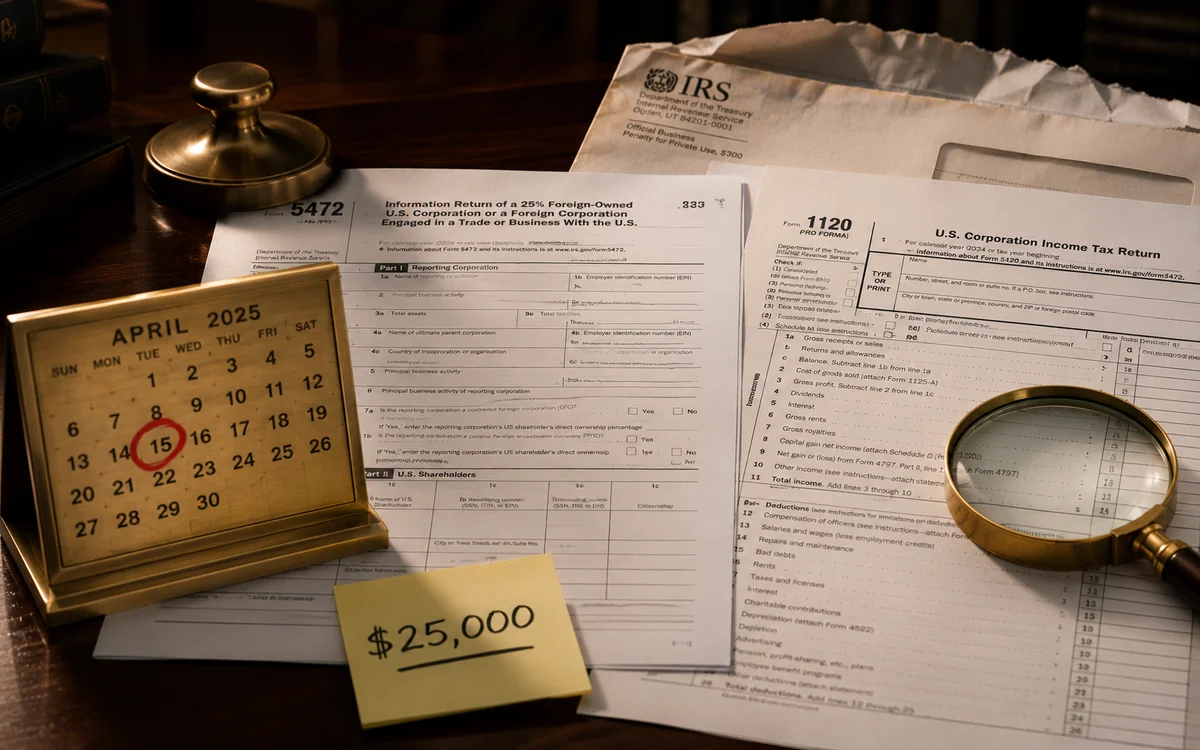

Form 5472 is the "Information Return of a 25% Foreign-Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business." In plain English — an information return about related-party transactions. Its purpose: give the IRS visibility into transactions between a US entity and its foreign related parties (the owner, the owner's relatives, the owner's foreign companies).

The legal basis is IRC §6038A and §6038C. As of 2017, Treasury Regulations expanded §6038A: a foreign-owned U.S. disregarded entity is treated as a corporation for the limited purposes of §6038A. In practice: if you, as a non-resident, own a single-member LLC — for Form 5472 purposes your LLC is treated as a corporation, even though IRS otherwise treats it as a disregarded entity.

Quick "do I have to file" test:

1. Your LLC is registered in the US.

2. You're the owner (or non-resident co-owners) holding 25%+ combined.

3. During the tax year there was at least one reportable transaction with you or a related party.

All three — yes? Form 5472 is required.

What counts as a "reportable transaction"

This is the most common misconception: "I had no operations, so I file nothing." In reality, reportable transactions include almost any movement of funds between the LLC and the owner:

- Capital contribution — you put money into the LLC (even the first starting deposit)

- Distribution — you took money out

- Payments between the LLC and a foreign related party (owner's other company, family member)

- Loan transactions (loan from owner to LLC or vice versa)

- Rent, royalties, fees

In other words: almost every operating foreign-owned SMLLC has at least one reportable transaction per year. Even if you only contributed $100 at the start and did nothing else — that's already a trigger.

Deadline and extension

Form 5472 is filed together with a pro forma Form 1120. The due date is the same as Form 1120's reporting corporation due date.

- For calendar year (January 1 – December 31): April 15 of the following year. So Form 5472 for 2025 is due April 15, 2026.

- Extension: Form 7004 filed by April 15 extends the deadline by 6 months — to October 15.

DE specifics: when filing Form 7004, use the Form 1120 code (Part I, line 1), and write "Foreign-owned U.S. DE" across the top of Form 7004. Without this label, IRS may misprocess the extension.

Pro forma 1120 — what it is and why

The least obvious part. Form 5472 cannot be filed standalone — it must be attached to Form 1120 (US Corporation Income Tax Return). But a foreign-owned U.S. DE does not owe corporate tax and has no normal income tax filing requirement. So you file a "pro forma" 1120 — a simplified version.

Per the official Instructions, on the pro forma 1120 only these are completed:

- Name and address of the foreign-owned U.S. DE

- Item B on the first page (EIN)

- Item E on the first page (date of incorporation, total assets)

All other 1120 fields (income, deductions, tax computation) are left blank. Pro forma 1120 is just a wrapper for Form 5472, so the IRS knows which entity 5472 belongs to.

Book a consultation with Edeal → calendly.com/orders-nexahub/meet-with-me

If you need to file Form 5472 for a past tax year, we have a dedicated team for it. Packet preparation takes 2–5 days. More: US company formation and support.

How and where to file

A foreign-owned U.S. DE cannot e-file. Two channels only: mail or fax.

Address for foreign-owned U.S. DE (from Instructions Rev. 12/2024):

Internal Revenue Service

1973 Rulon White Blvd, M/S 6112

Attn: PIN Unit

Ogden, UT 84201

Fax

Fax: 855-887-7737 (minimum 300 DPI). The document must be clear — IRS rejects unreadable faxes.

What goes in the packet

- Form 1120 (pro forma — only name, address, item B, item E completed)

- Form 5472 (fully completed)

- Across the top of Form 5472 write "Foreign-owned U.S. DE" (per Instructions)

The $25,000 penalty — in detail

Under IRC §6038A(d) and related regulations:

- $25,000 — for failure to file Form 5472 (or filing in the wrong form).

- Additional $25,000 — if the failure continues more than 90 days after IRS notification.

- Applied per tax year separately. Skip 3 years — theoretically $75,000+ in base penalties.

In practice IRS doesn't always assess the maximum, but you cannot count on leniency. Penalty abatement is possible by demonstrating "reasonable cause" — but that's a separate procedure requiring a written explanation, and it doesn't always work.

Form 5471 vs Form 5472 — don't confuse them

These two are regularly confused because the numbers look similar. The difference is fundamental:

- Form 5472 — for a US entity (LLC, corporation) owned by a foreigner. Purpose: show IRS transactions between the US entity and its foreign owner.

- Form 5471 — for a US person who owns a foreign corporation. Purpose: show IRS that a US person controls a CFC (controlled foreign corporation).

If you're a non-resident with a US LLC: your world is Form 5472. Form 5471 applies to Americans with companies in Estonia, UAE, and so on.

What to do if you've already missed it

If you realize you haven't filed Form 5472 for past years, three paths:

First. File late on your own, without explanation. IRS may assess the penalty automatically, and then you'd have to fight it via abatement.

Second. File with an attached Reasonable Cause Statement — a written explanation of why the form wasn't filed on time. If the cause is found convincing (e.g., you just learned of the requirement, no fraud intent), the penalty can be waived. This works more often than you'd expect.

Third. If the LLC isn't needed anymore — consider dissolving. Closing the LLC with a final 5472 for the last active year is a "cold" path, but sometimes the most cost-effective one.

Common mistakes

"I had $0 revenue — nothing to file." A capital contribution at startup is already a reportable transaction. Filing is mandatory.

E-filing through TurboTax or other consumer service. Foreign-owned DE does not e-file — only mail or fax.

Filing only Form 5472 without 1120. They go together. Without pro forma 1120, IRS returns the form as incomplete.

Filling out the full 1120. Pro forma 1120 is name, address, item B, item E. The rest stays blank. If you fill in income/deductions, IRS may demand a real corporate return with corporate tax payment.

Forgot the "Foreign-owned U.S. DE" label on Form 5472 or 7004. This is a meaningful processing error.

File Form 5472 without the penalty?

At Edeal we file Form 5472 plus pro forma 1120 for our clients annually. Standard packet preparation — 2–5 days. If you're already late, we'll help draft a Reasonable Cause Statement.

- Instructions for Form 5472 (Rev. 12/2024) — IRS.gov

- About Form 5472 — IRS.gov

- International Information Reporting Penalties — IRS.gov

- Instructions for Form 1120 (2025) — IRS.gov